In an increasingly globalized economy, businesses seeking competitive advantage need to reevaluate how they facilitate cross-border transactions for their customers. The cross-border payments infrastructure—a $194 trillion market in 2024 with projections to reach $320 trillion by 20321 represents both a significant challenge and a strategic opportunity for financial service providers.

The Hidden Complexity Behind Every International Transfer

For financial institutions, payment service providers, and enterprises with global operations, cross-border payment capabilities are no longer a supplementary offering—they're a core strategic asset. Organizations that can overcome the three primary friction points in international transfers gain significant competitive advantages:

- Speed inefficiencies: Traditional transfers taking 2-5 days create opportunities for providers offering same-day or real-time alternatives

- Cost opacity: Hidden fees of 3-7% represent margin that innovative providers can disrupt

- Access limitations: The 1.4 billion unbanked adults worldwide2 represent an untapped market for inclusive payment solutions

Let's examine the four key methods that power today's cross-border payments ecosystem, with real-world examples that highlight their practical applications.

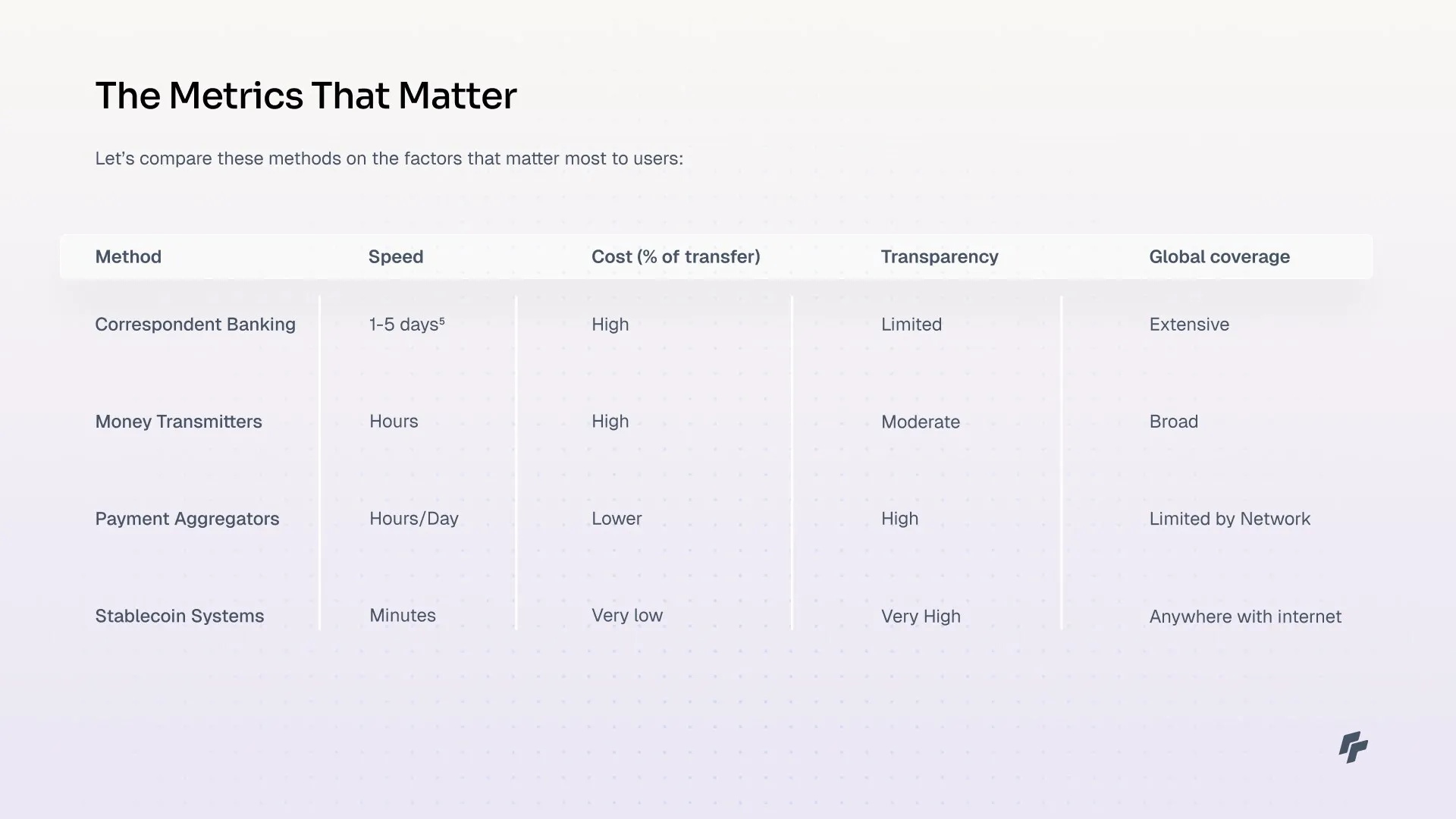

1. Correspondent Banking Networks: The Traditional Highway

Correspondent banking exists as the backbone of international finance today.

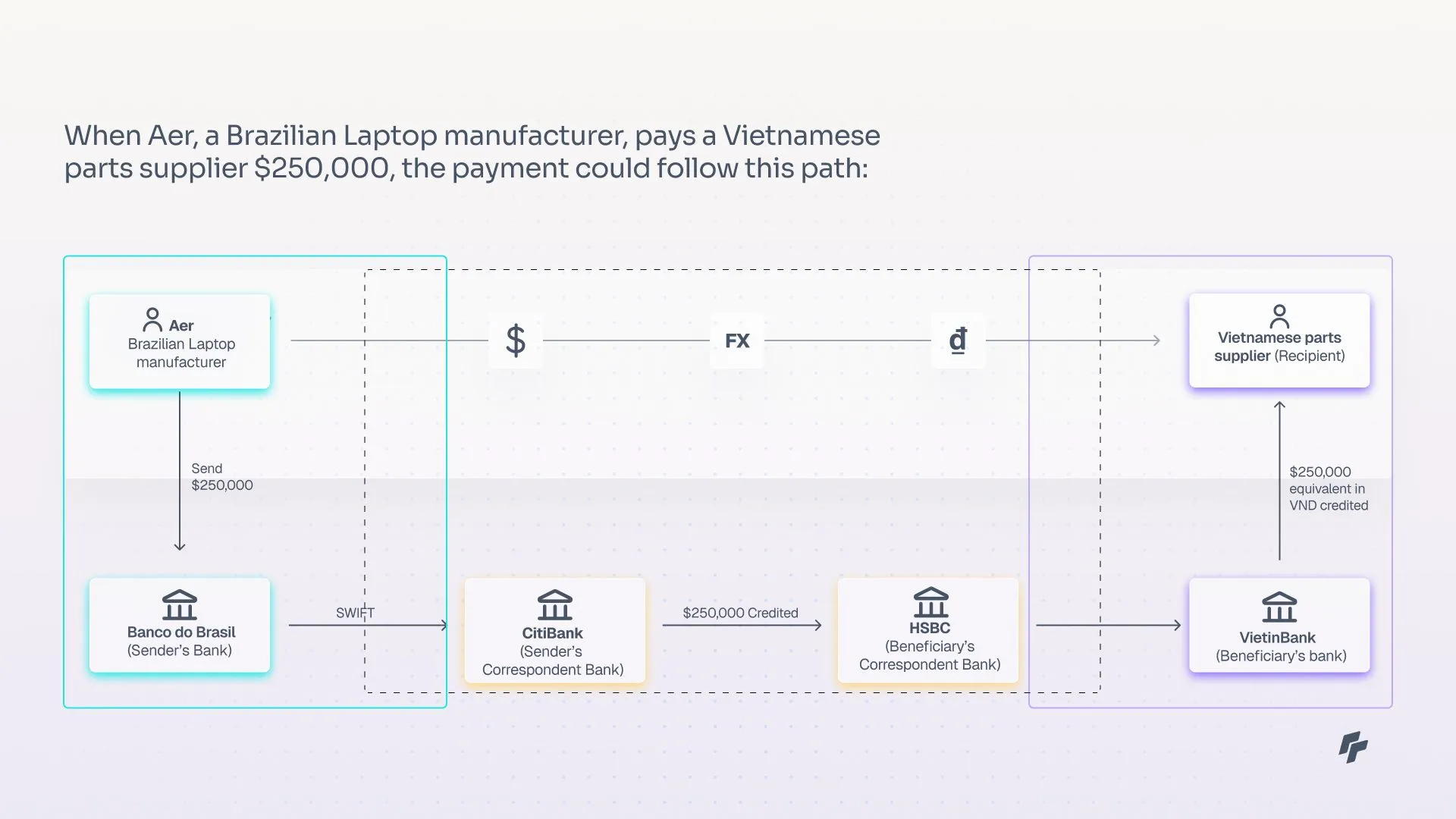

How it actually works: When a Brazilian company needs to pay a Vietnamese supplier, their respective banks likely don't have a direct relationship. Instead, they rely on a chain of correspondent banks—often including a major international bank like JPMorgan Chase or HSBC—that maintain accounts with each other.

Example: When Aer, a Brazilian Laptop manufacturer, pays a Vietnamese parts supplier $250,000, the payment could follow this path:

- Aer instructs Banco do Brasil to send $250,000 to the supplier's account at VietinBank

- Banco do Brasil sends a SWIFT message to their U.S. correspondent (Citibank)

- Citibank debits Banco do Brasil's nostro account and credits HSBC's account (VietinBank's correspondent)

- HSBC sends a message to VietinBank to credit the supplier's account in Vietnamese dong

2. Money Transmitter Networks: The Retail Network

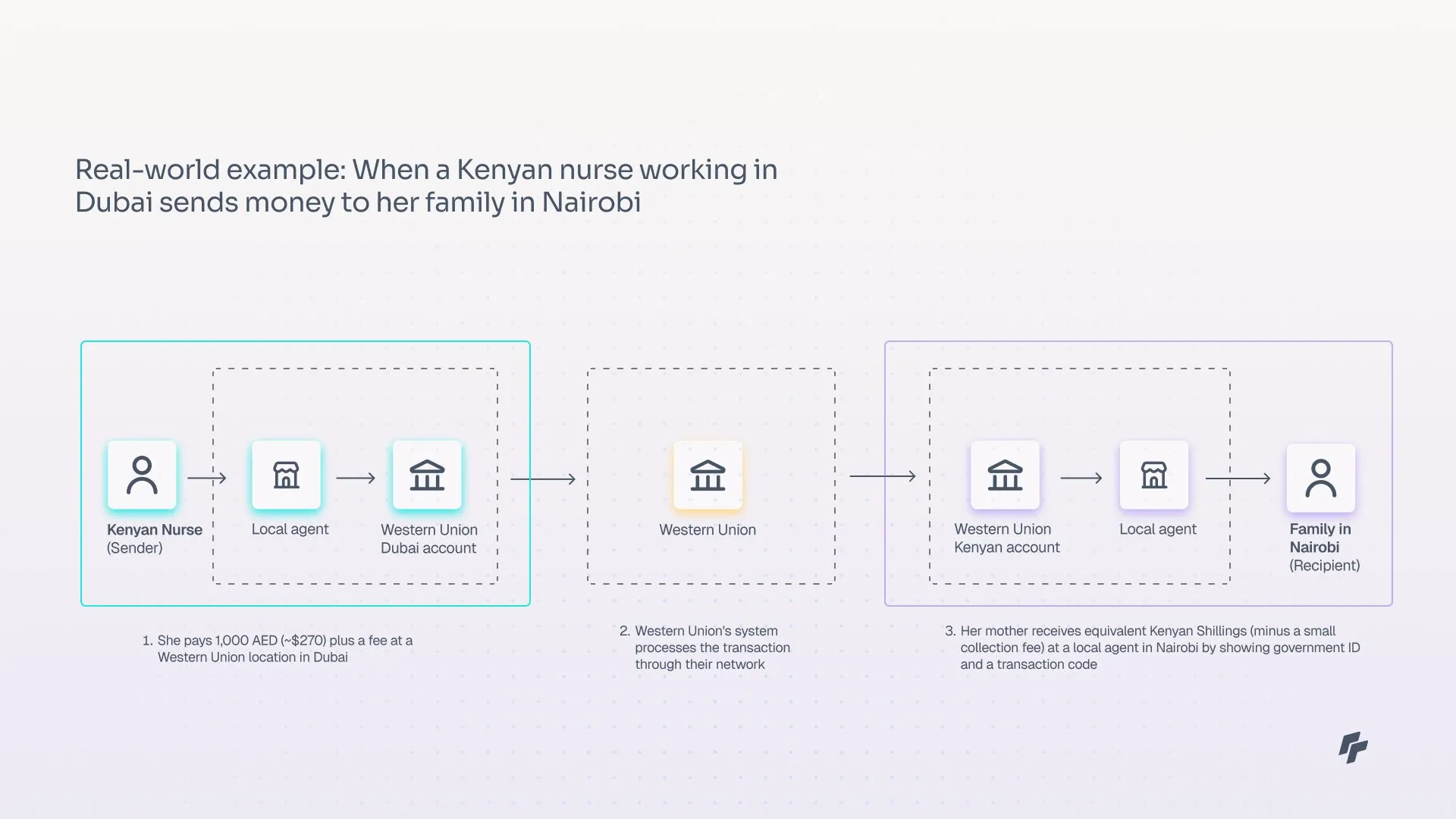

Money transmitters like Western Union and MoneyGram operate over 200 countries3, serving as critical infrastructure for communities with limited banking access.

How it actually works: These services maintain pre-funded accounts in various countries, allowing them to receive funds in one location and disburse equivalent amounts in another without actually moving money across borders for each transaction.

Real-world example: When a Kenyan nurse working in Dubai sends money to her family in Nairobi:

- She pays 1,000 AED (~$270) plus a fee at a Western Union location in Dubai

- Western Union's system processes the transaction through their network

- Her mother receives equivalent Kenyan Shillings (minus a small collection fee) at a local agent in Nairobi by showing government ID and a transaction code

3. Payment Aggregator Models: The Digital Optimizers

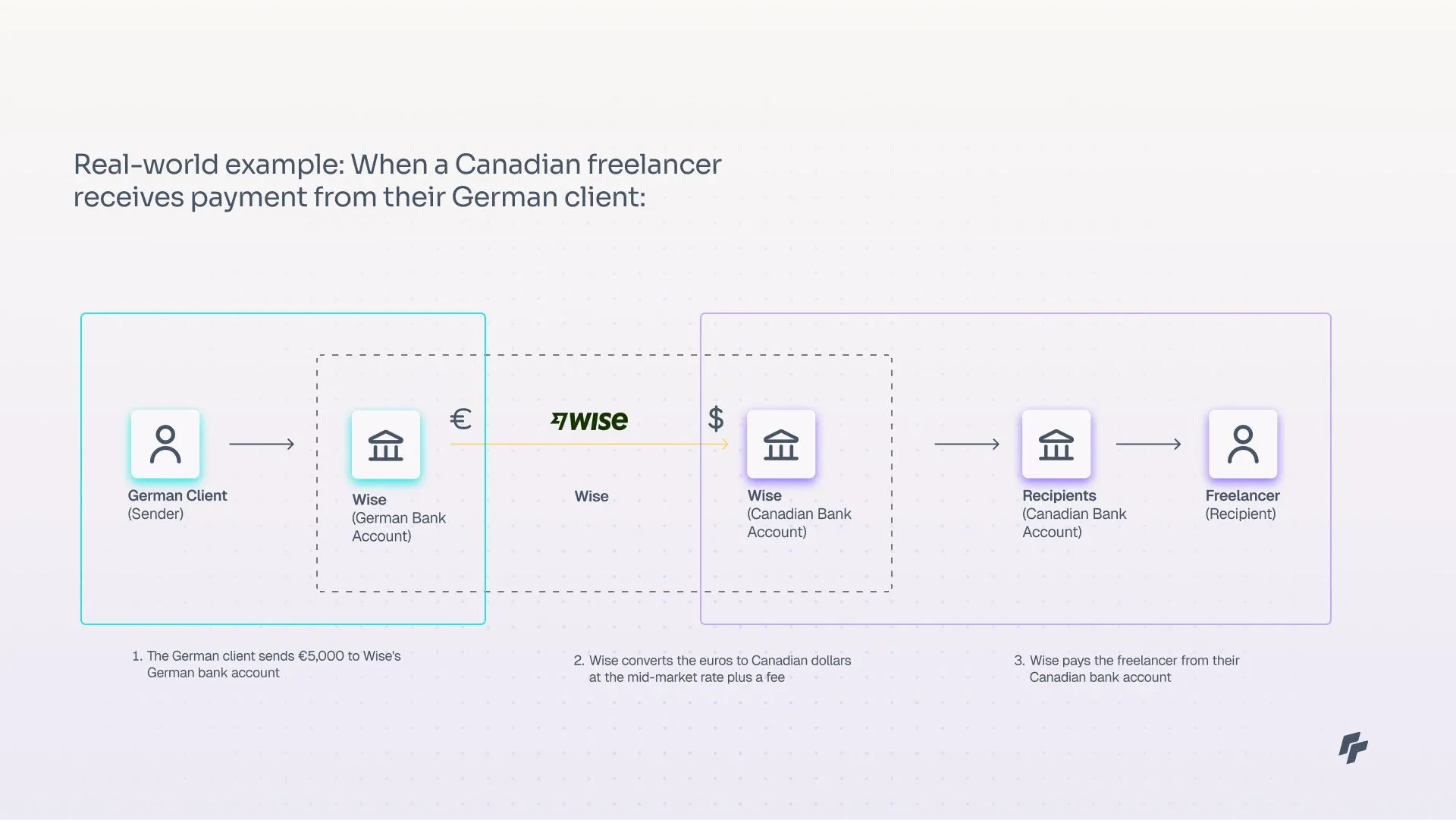

Companies like Wise and Revolut have demonstrated that purpose-built payment infrastructure can significantly outperform traditional banking rails on cost and user experience, particularly for digital-first customers.

How it actually works: Unlike money transmitters that focus on cash, these platforms link directly to bank accounts across multiple countries. Their innovation lies in using a matching system—pairing outgoing and incoming transfers in the same currency to minimize actual cross-border movements.

Real-world example: When a Canadian freelancer receives payment from their German client:

- The German client sends €5,000 to Wise's German bank account

- Wise converts the euros to Canadian dollars at the mid-market rate plus a fee

- Wise pays the freelancer from their Canadian bank account

4. Digital asset Infrastructure: The Emerging Fast Lane

The digital asset ecosystem—comprising stablecoins, tokenized deposits, and CBDCs—represents the frontier of cross-border payment innovation. Stablecoins alone settled $10.8 trillion worth of transactions in 2023, with $2.3 trillion attributed to organic payment activities including cross-border remittances.4 For forward-looking financial institutions, this infrastructure represents an opportunity to dramatically reduce settlement costs by 70-90% while enabling near-instantaneous processing times—a competitive advantage that early adopters are already leveraging to capture market share from traditional providers.

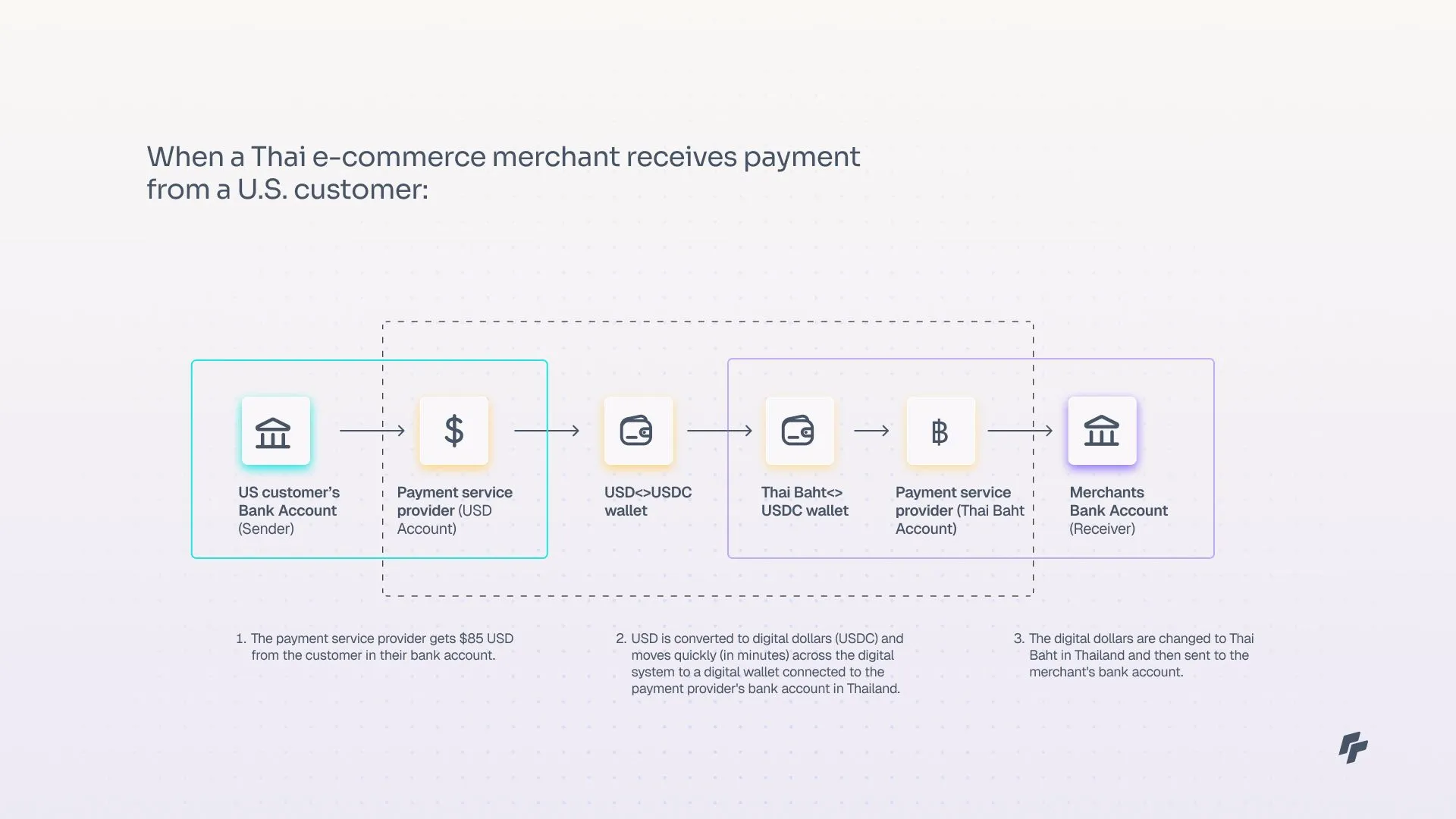

How it actually works: These systems use immutable ledgers like blockchain technology to move value almost instantly across borders, with tokenized currencies like stablecoins or CBDCs serving as a bridge currency that can be quickly converted to local fiat currencies on either end.

Example: When a Thai e-commerce merchant receives payment from a U.S. customer:

- The payment service provider gets $85 USD from the customer in their bank account and changes it to digital dollars (USDC)

- These digital dollars move quickly (in minutes) across the digital system to a digital wallet connected to the payment provider's bank account in Thailand

- The digital dollars are changed to Thai Baht in Thailand and then sent to the merchant's bank account

Strategic Market Developments to Monitor

Growing adoption and regulatory clarity are creating unprecedented opportunities in the stablecoin/CBDC cross-border payments landscape:

- Institutional Adoption: Major financial institutions and central banks are rapidly embracing digital currency innovation. According to the Atlantic Council CBDC Tracker, 134 countries and currency unions representing 98% of global GDP are now actively exploring CBDCs.6 China's digital yuan has already processed over cumulative $7.4 trillion in transactions by mid 20247, with cross-border corridors established between Hong Kong, Thailand, and the UAE. Meanwhile, private sector leaders are exploring stablecoin capabilities.

- Regulatory Evolution: Regulators have pivoted from cautious skepticism to proactive frameworks supporting innovation. Singapore's Monetary Authority (MAS) launched Project Guardian in 2022, collaborating with JPMorgan, DBS Bank, and other financial institutions to pilot asset tokenization and assess its transformative potential for financial markets.8 In the United States, the New York Department of Financial Services has established concrete guidance for dollar-backed stablecoins,9 while the proposed GENIUS Act aims to create a comprehensive federal framework for stablecoin issuers, providing regulatory certainty that could accelerate institutional adoption.10

The Bottom Line

The cross-border payments landscape is undergoing fundamental restructuring, creating opportunities for forward-thinking financial institutions to deliver exceptional value while capturing market share. Organizations that succeed will approach payments not merely as a necessary service but as a strategic differentiator.

For executives overseeing payment strategy, the key takeaway is that modernizing cross-border infrastructure isn't just a technical requirement—it's a business imperative. As faster, cheaper, and more transparent alternatives continue emerging, customer expectations are being fundamentally reset. The financial institutions that thrive will be those that recognize this shift early and position themselves not just as participants in the global payment ecosystem, but as innovators driving its evolution.

Sources

- World Bank. “Financial Inclusion”: https://www.worldbank.org/en/topic/financialinclusion/overview#:~:text=The%20expansion%20of%20digital%20financial,owning%20an%20account%20by%202021.

- Western Union: https://www.westernunion.com/blog/en/send-money-around-the-world-with-the-brand-you-trust/?cust_src=organic_search

- Coinbase. “Stablecoins and the New Payments Landscape”: https://www.coinbase.com/en-gb/institutional/research-insights/research/market-intelligence/stablecoins-new-payments-landscape

- PwC. “The evolving landscape of cross-border payments”: https://www.pwc.in/assets/pdfs/consulting/financial-services/fintech/point-of-view/pov-downloads/the-evolving-landscape-of-cross-border-payments.pdf

- Atlantic Council CBDC tracker: https://www.atlanticcouncil.org/cbdctracker/

- Forbes. “A 2025 Overview Of The E-CNY, China’s Digital Yuan": https://www.forbes.com/sites/digital-assets/2024/07/15/a-2024-overview-of-the-e-cny-chinas-digital-yuan/

- Monetary Authority of Singapore. “Project Guardian”: https://www.mas.gov.sg/schemes-and-initiatives/project-guardian

- New York State Department of Financial Services. “Virtual Currency Guidance”: https://www.dfs.ny.gov/industry_guidance/industry_letters/il20220608_issuance_stablecoins

- Congress.Gov “GENUIS act of 2025” https://www.congress.gov/crs-product/IN12522

.webp)

.avif)